Future of Bank Mergers in India- A Legal Perspective

- sonalimukhia2002

- Oct 25, 2025

- 5 min read

Author: Kanishika Talwar, St. Soldier College of Law

INTRODUCTION

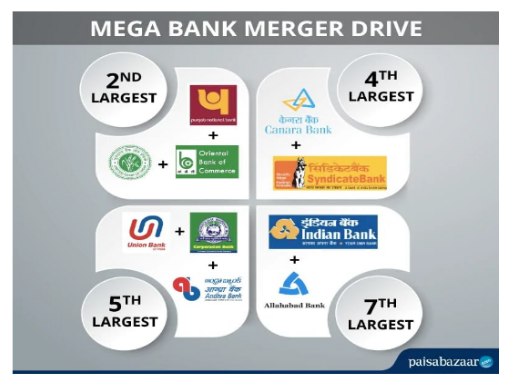

Did you know that in the past ten years, India has experienced more than two dozen significant bank mergers? From the massive State Bank of India merging with its affiliate banks, to the 2019 consolidation that reduced ten public sector banks down to four! These are not merely corporate changes; they represent fundamental transformations in how credit is generated, how capital circulates, and how economic power is allocated. Think of it as India rewiring its entire financial nervous system and yet, beneath the polished press statements lies a web of intricate legal challenges. Issues relating to Competition Law, Employee Rights, Depositor Protections, and Regulatory Overlaps could determine the success or failure of these transactions.

Why is this important to you? Because whether you’re using your UPI, seeking a student loan, or trading in stocks, the evolving structure of Indian banks has a direct impact on you. Bank mergers are where the prudence of The Reserve Bank of India intersects with the laws established by Parliament and the vigilant oversight of the judiciary. This article delves into that legal framework, analyzing the evolution of India’s merger laws, the loopholes they reveal, and how upcoming transactions may not only transform our financial environment but also our legal system.

So, here’s the pressing question: Are India’s bank mergers reinforcing a more robust financial structure or setting the stage for the next significant legal upheaval?

BANK MERGERS: THE LEGAL BEDROCK

Bank mergers in India are far from casual arrangements. They’re governed by a web of laws such as, The Banking Regulation Act, 1949, The Companies Act, 2013, The Competition Act, 2002, and RBI-specific guidelines. Public sector banks (PSBs) have an extra layer, government notifications under The Banking Companies (Acquisition and Transfer of Undertakings) Actsand Cabinet approval. Every merger is essentially a chess game between The Parliament, The RBI and The Ministry of Finance.

RBI plays numerous roles such as, approves schemes, evaluates financial soundness, protects depositor’s interests etc.

Competition Commission of India (CCI): Checks anti-competitive effects and market dominance.

Courts and Tribunals: Step in if employees, shareholders, or third parties challenge the merger.

Without these legal checks, mergers could risk financial instability, unfair treatment of stakeholders, and breaches of depositor trust.

WHY INDIA WENT ALL-IN ON CONSOLIDATION?

Following 2010, the Indian banking sector encountered an increase in non-performing assets, banks lacking sufficient capital, and greater competition from global companies. Smaller public sector banks found it difficult to remain viable, prompting the government to implement a consolidation strategy. The objectives of this approach were:

Efficiency: Optimizing technology systems and risk management to lower costs.

Capital Strength: Consolidated banks establish bigger balance sheets that can support significant infrastructure initiatives.

Global Credibility: Placing India’s banks on par with international financial leaders such as HSBC or JP Morgan.

Nevertheless, this rapid consolidation raised legal challenges because the existing framework was not originally designed for extensive mergers. Modifications, government statements, and judicial oversight have become essential to uphold the legitimacy and equity of the process.

THE LEGAL MINEFIELDS NOBODY TALKS ABOUT

Although mergers may seem straightforward on paper, in reality however, they resemble a legal demolition derby, every stakeholder striving to safeguard their interests.

Employee Rights & Unions: Pursuant to the Industrial Disputes Act and banking service regulations, employees have the right to legally contest transfers, redundancy plans, or modifications to benefits. Courts frequently weigh the need for organizational efficiency against the protections afforded to employees.

Shareholder Protection: Minority shareholders are entitled, under The Companies Act and SEBI guidelines, to challenge issues related to valuation, swap ratios, and disclosure practices.

Data Privacy & Cyber security: The integration of banks necessitates the merging of extensive customer databases, which brings forth compliance challenges in light of India's evolving data protection laws e.g. Digital Personal Data Protection Act, 2023

Competition Issues: If a merger gives one bank excessive regional or sectorial dominance, the CCI can impose conditions or even block the deal.

Neglecting these legal factors invites not only litigation, but also risks reputational harm and regulatory sanctions.

THE JUDICIARY’S QUIET BUT CRITICAL ROLE

Indian courts infrequently outright block bank mergers, but their interpretations of laws influence the legal framework. For instance:

SBI & Associate Banks Merger: High Courts dismissed the majority of petitions yet emphasized the importance of procedural fairness regarding employee relocations and notification of stakeholders.

Kotak Mahindra–ING Vysya Merger: Demonstrated how private banks handle RBI approvals and shareholder rights through meticulous legal structuring.

IDBI–LIC Case: Highlighted regulatory conflicts that arise when insurers acquire controlling stakes in banks, raising questions on corporate governance and public interest.

These judicial interventions create a framework of soft law; unseen yet influential guidelines for upcoming mergers.

FUTURE TRENDS: THE DIRECTION OF LEGAL DEVELOPMENTS

The upcoming decade is expected to witness mergers extending beyond conventional Public Sector Banks (PSBs). Significant trends anticipated to transform legal frameworks include:

Fintech Mergers: Collaborations between banks and fintech companies will introduce fresh legal challenges related to digital assets, cyber security, and international data transfers

ESG & Compliance Demands: Investors are increasingly seeking thorough evaluations of environmental, social and governance risks prior to sanctioning transactions.

Inter-Sector Mergers: Non-Banking Financial Companies (NBFCs) merging with banks within an evolving regulatory landscape may require the creation of entirely new statutes.

Enhanced Depositor Protection: The changing regulations from The Deposit Insurance and Credit Guarantee Corporation (DICGC) will address risks associated with institutions deemed "too big to fail."

THE SIGNIFICANT LEGAL DILEMMA: STABILITY vs. MONOPOLY

With the merging and consolidation of banks, regulators face a delicate balancing act:

Excessively Fragmented: If the banking sector is excessively fragmented, it can lead to weak institutions, inadequate credit provision, and increased susceptibility to crises.

Excessively Concentrated: Conversely, if the sector is overly concentrated, it risks monopolistic behavior and the potential for systemic risk if a single institution fails.

Future changes to The Banking Regulation Act and Competition Act are expected to incorporate core principles such as systemic risk evaluations and depositor protection measures.

CONCLUSION

Bank mergers in India represent more than just corporate reorganizations; they act as legal experiments that shape the financial fabric of the nation. Each consolidation, ranging from SBI’s significant merger to the 2019 PSB integrations has tested the limits of banking regulations, competition policies, and judicial oversight. The upcoming decade is expected to intensify this dynamic, with digital banks, fintech companies, and NBFCs entering the merger landscape.

For legislators and regulatory bodies, the challenge lies in finding balance, creating banks that can support a $5-trillion economy while ensuring that these institutions do not become systemic risks. For legal practitioners, there are abundant opportunities within litigation, policy formulation, and compliance frameworks.

The key takeaway? The future of India’s banking sector will be written not just in financial statements, but also in courtrooms, legislative processes, and regulatory decisions. Whether we establish a resilient financial institution or a delicate oligopoly, hinges on how boldly and wisely we adapt our legal framework today.

References

Deposit Insurance and Credit Guarantee Corporation Act, No. 47 of 1961 (India Code), available at https://www.indiacode.nic.in/handle/123456789/1565.

Industrial Disputes Act, No. 14 of 1947 (India Code), available at https://www.indiacode.nic.in/handle/123456789/1534.

Kotak Mahindra Bank Ltd.–ING Vysya Bank Ltd. Scheme of Amalgamation, Bombay High Court Order (2015), available at https://www.rbi.org.in/scripts/BS_PressReleaseDisplay.aspx?prid=32806.

Life Insurance Corp. of India Acquiring IDBI Bank Ltd. (RBI Approval / SEBI Order, 2019), available at https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=45659.

Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015 (as amended May 17, 2023), available at https://www.sebi.gov.in/legal/regulations/oct-2015/sebi-listing-obligations-and-disclosure-requirements-regulations-2015-last-amended-on-may-17-2023_37269.html.

State Bank of India & Ors. v. All India State Bank of Bikaner & Jaipur Employees Union & Ors., (2017), available at https://indiankanoon.org/doc/125682401/.